Non-ferrous

Non-ferrous

Base Metals

Rare Earth

Scrap Metals

Minor Metals

Precious Metals

New Energy

Price CenterDatabaseProReportsEventsCar Insight

Language:

Language:

View SMM aluminum product quotes, data, and market analysis

Order and view SMM metal spot historical prices

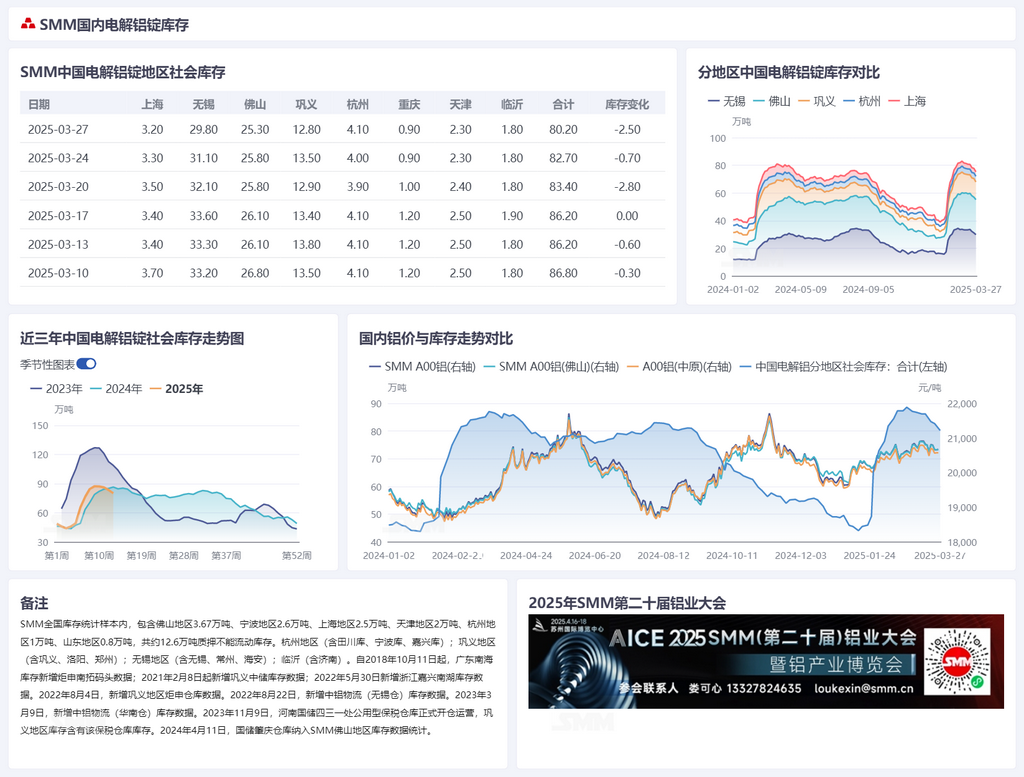

Approaching the end of March, domestic aluminum ingot inventory dropped sharply by 25,000 mt mid-week, nearing the 800,000 mt mark.According to SMM statistics, on March 27, the inventory of primary aluminum ingots in major domestic consumption areas was 802,000 mt, of which the circulating inventory was 676,000 mt, down 25,000 mt from Monday this week and down 32,000 mt WoW from last Thursday.This phenomenon was mainly driven by the steady increase in outflows from warehouses. Over the past week, outflows from major consumption areas were 128,400 mt, up 1,300 mt WoW, with weekly outflows since March remaining around 130,000 mt.

According to SMM, due to increased demand from the automotive and PV sectors in east China, restocking demand rose significantly this week, leading to a sharp decline of 13,000 mt in inventory in Wuxi mid-week. Although procurement in Gongyi remained primarily driven by rigid demand, supply and demand conditions improved this week, with inventory decreasing by 7,000 mt mid-week. The rapid inventory consumption was closely related to the reduction in in-transit and arrival volumes: arrivals in Wuxi decreased by over 10,000 mt this week, while Foshan and Gongyi remained relatively stable. Additionally, approaching holidays such as Qingming Festival, reduced transportation capacity led to a short-term increase in transportation costs, especially with a decline in trucking volumes in Yunnan and Guangxi this week, which facilitated warehouse inventory consumption.SMM expects that domestic aluminum ingot inventory will continue its destocking trend in the first half of April, potentially pulling back to around 750,000 mt by mid-April.

In the spot aluminum market, purchasing as needed remained the main trend this week, with some leading enterprises stockpiling mid-week. Discounts in east China narrowed, mainly due to continued destocking and reduced arrivals in Wuxi, coupled with strong downstream demand for aluminum in PV and NEVs. As of Thursday this week, the discount of SMM A00 spot prices against the April contract was 10 yuan/mt, narrowing by 30 yuan/mt WoW from last Thursday. Trading in central China was moderate, with aluminum prices rising today and strong market sentiment. As of Thursday this week, the discount of SMM Central China A00 against the April contract was 110 yuan/mt, narrowing by 40 yuan/mt WoW from last Thursday. In south China, discounts narrowed early this week due to monthly long-term contract delivery needs, but demand weakened later, and suppliers' willingness to recoup funds at month-end led to relatively ample market circulation. The overall market performance was stable this week, with discounts narrowing by 10 yuan/mt WoW to 35 yuan/mt. In the short term, despite the seasonal peak season background, aluminum demand increased, and upward momentum in aluminum prices remained. However, due to limited downstream acceptance of high prices, spot premium growth was slow. Model predictions indicate that the average premium/discount range for SMM A00 aluminum is [-30, -5] yuan/mt, with a center value of -15 yuan/mt, an extreme price range of [-70, 40] yuan/mt, a normal price range of [-35, 0] yuan/mt, and a conservative price range of [-25, -10] yuan/mt.

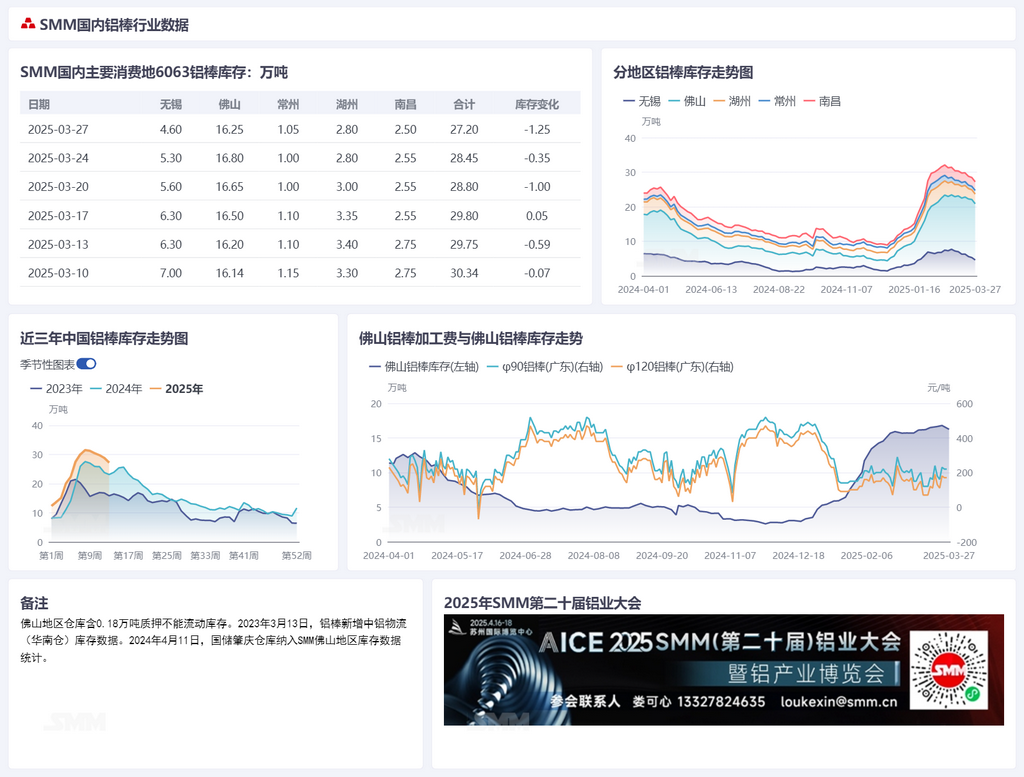

Regarding aluminum billet inventory,according to the latest SMM data, as of March 27, 2025, domestic aluminum billet social inventory was 272,000 mt, down 16,000 mt WoW from last Thursday and down 12,500 mt from Monday this week. In terms of outflows, with the deepening of the "Golden March, Silver April" consumption peak season, extrusion orders performed commendably, and coupled with the pullback in aluminum price center, last week's aluminum billet outflows reached 62,200 mt, hitting a yearly high and driving a decline in aluminum billet inventory. This week, aluminum prices continued to adjust, and with downstream consumption fully released at current aluminum prices, aluminum billet destocking remained stable. SMM believes that the logic of marginal strengthening in terminal restocking momentum remains unchanged, and domestic aluminum billet inventory is expected to continue a steady decline in the first half of April, potentially pulling back to the 200,000-250,000 mt range in April.

Weekly fundamentals showed positive supply and demand performance, with SHFE aluminum maintaining range adjustments and downstream purchasing sentiment remaining favorable. Aluminum billet inventory is in a continuous destocking trend, with current market supply remaining relatively ample, and suppliers intend to raise processing fees while demand-side maintains a bargain-down purchasing rhythm. This week, Foshan aluminum billet supply

is expected to tighten, with good trading conditions. Aluminum billet market quotes were 160/210, up 30 from last Thursday; specific models of aluminum billets in Wuxi experienced shortages, with processing fees quoted at 150/200, down 30 from last Thursday; Nanchang market sentiment was moderate, with processing fees quoted at 150/200, up 30 from last Thursday. (Unit: yuan/mt)

On the demand side for aluminum billets,the operating rate in the aluminum extrusion industry rose slightly by 1 percentage point WoW to 61%, with sub-sectors continuing to diverge.In industrial extrusions, leading automotive extrusion enterprises maintained an 80%+ operating rate with orders from the NEV industry chain. However, according to SMM surveys, some small and medium-sized building material enterprises that previously ventured into industrial extrusions reported that automotive extrusions, due to complex process certifications and significant equipment investments, are now increasingly concentrated in leading enterprises. Some SMEs, facing severe product homogenization, have seen idle industrial production lines this week. In PV extrusions, despite continued pressure on processing fees, mainstream PV extrusion enterprises maintained full production due to component manufacturers' concentrated delivery periods in March-April. In construction extrusions, some enterprises reported that government special bond projects (such as high-speed rail and industrial parks) have boosted public construction orders, with construction extrusion operating rates slightly increasing this week. However, demand for civilian building materials remains suppressed by slower real estate completions, and operating rates for window, door, and aluminum formwork extrusion enterprises remain low. SMM will continue to track inventory destocking rhythms during the traditional peak season, focusing on the efficiency of demand transmission from NEVs and PV installations and the actual boost from local government special bonds on infrastructure projects.

For queries, please contact Lemon Zhao at lemonzhao@smm.cn

For more information on how to access our research reports, please email service.en@smm.cn